Federal student loan policies may change over time as a result of federal legislation or Department of Education guidance. This page provides the most current information about upcoming changes to federal loan eligibility and what they may mean for Community College System of New Hampshire students.

We are committed to sharing clear, accurate information and supporting students as they plan ahead.

Upcoming Federal Loan Policy Changes

Effective Beginning with the 2026–2027 Academic Year

Beginning in the 2026–2027 academic year (CCSNH is a header college, 2026-2027 start Summer 2026), federal rules will update how federal loan eligibility is determined. These changes apply nationally and are not specific to the Community College System of New Hampshire.

Key changes include

- Loan based on annual enrollment

Students enrolled less than full time will see a reduced maximum federal loan amount. Loan eligibility will be calculated based on the number of credits in which a student is enrolled.

This change applies regardless of prior borrowing and does not have legacy provisions. - Parent PLUS Loan Annual and Aggregate Limits

The Federal Parent PLUS loans will be capped at a maximum of $20,000 per student per academic year, with a lifetime aggregate limit of $65,000 per student. These limits apply to all parents combined per dependent undergraduate student beginning in the 2026-2027 academic year.

Legacy provisions may apply for some current students who remain enrolled in the same program. See “What Is Not Changing” below.

What Is Not Changing

While some aspects of federal loan eligibility are changing, several important programs will continue.

- Federal Direct Loans will remain available to eligible students.

- Legacy Parent PLUS Borrowing can continue under prior borrowing limits tied to the cost of attendance minus other financial aid provided the student or parent borrower has:

- Borrowed a federal direct loan before July 1, 2026 while the dependent student was enrolled

All legacy provisions are limited to the shorter of:

- The remaining length of the program, or

- Three additional years.

For many students — particularly those enrolled full time — there may be little or no immediate impact.

What Students Should Know

CCSNH will continue to provide students with an anticipated full time loan amount as part of the financial aid process based on expected enrollment.

- Final loan eligibility is confirmed after course registration and review of cost of attendance.

- For some students, loan eligibility may look different than in prior years.

- For others, eligibility may remain largely the same.

Detailed and individualized information will be shared when CCSNH receives the final regulation from the US Department of Education.

2026 – 2027 Loan Reduction:

See Chart below for calculation:

| Credit hours for Academic year | Number of Credits considered Full Time for academic year | % of Eligible Loan limit* |

| 24 | 24 | 100% |

| 23 | 24 | 96% |

| 22 | 24 | 92% |

| 21 | 24 | 88% |

| 20 | 24 | 83% |

| 19 | 24 | 79% |

| 18 | 24 | 75% |

| 17 | 24 | 71% |

| 16 | 24 | 67% |

| 15 | 24 | 63% |

| 14 | 24 | 58% |

| 13 | 24 | 54% |

| 12 | 24 | 50% |

| 11 | 24 | 46% |

| 10 | 24 | 42% |

| 9 | 24 | 38% |

| 8 | 24 | 33% |

| 7 | 24 | 29% |

| 6 | 24 | 25% |

* Annual loan limits may be affected by Withdrawal and Dropping course after disbursement.

Waiting Further guidance regarding loan proration from the Department of Education.

FAQ: Summer Loans and Annual Loan Limits

Subject to change based on final federal regulations.

Starting in the 2026–2027 award year, your annual loan limit may be reduced proportionally if you are enrolled less than full-time (24 credits annually).

1. What are the annual loan limits?

Dependent Students:

- First Year: $5,500

- Second Year: $6,500

Independent Students:

- First Year: $9,500

- Second Year: $10,500

2. What changed from last summer to this summer, and how much will I receive?

The primary change is how the annual loan limit is distributed.

Previously, CCSNH divided the annual loan limit evenly across three semesters. Beginning this summer, students enrolled in at least 6-8 credits will be awarded up to 25% -33% of their annual loan limit for the summer term. The remaining 75%-67% will be split between the fall and spring semesters.

Estimated Summer Loan Amounts at 25%

Dependent Students:

- First Year: $5,500 × 25% = $1,375

- Second Year: $6,500 × 25% = $1,650

Independent Students:

- First Year: $9,500 × 25% = $2,375

- Second Year: $10,500 × 25% = $2,625

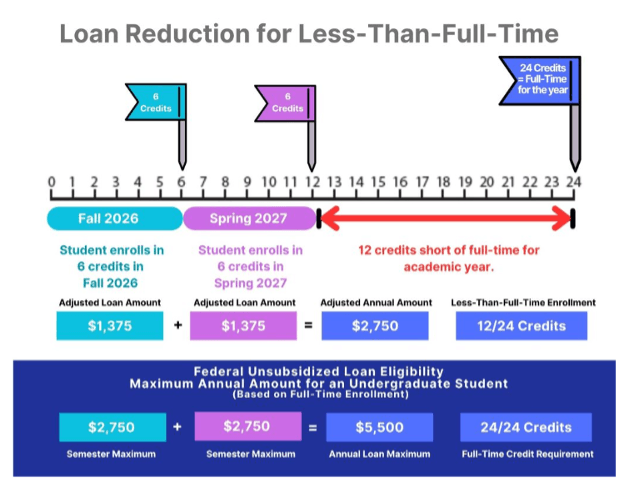

3. What if I am enrolled in 12 credits for fall and 12 credits for spring?

Students enrolled in 12 or more credits (full-time) in a semester may be eligible for up to 50% of their annual loan limit for that term.

If enrolled in 6 credits (half-time), eligibility would typically be up to 25% of the annual loan limit for that semester.

4. What happens if I drop a course?

Your loan eligibility is directly tied to your enrollment level. If you drop below full-time or half-time status, your loan amount may be reduced or canceled accordingly.

5. If I am enrolled in 3 credits in the first half and 3 credits in the second half, when will my loan disburse?

Loan funds will not be disbursed until the college confirms your attendance in the second half course.

6. What happens if I fail a course?

Still awaiting guidance

7. Examples:

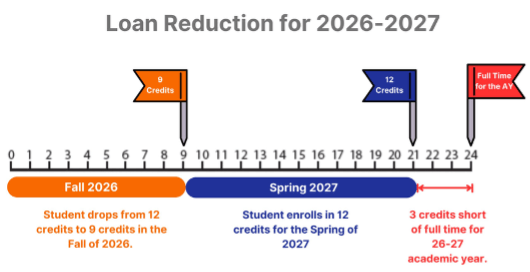

Fall/Spring Fulltime to start and drops:

Full-Time Status is 24 credits for the academic year (12 credits per semester)

A student who drops to 9 credits in the fall semester and maintains 12 credits for the spring semester will be 3 credits short of being considered full time for the academic year. Due to dropping the 3 credits the student federal loans must be reduced.

Fall/Spring Part-Time Fall and Spring:

Full-Time Status is 24 credits for the academic year (12 credits per semester)

A first-year student enrolled in 6 credits in the fall semester and enrolls in 6 credits in the spring semester will be enrolled in 12 credits, short of being considered full time for the academic year which is 24 credits.